A bank locker protects your valuables. But how much does it actually protect if something goes wrong?

In February last year, a family in Visakhapatnam discovered their bank locker had been broken into. Inside were three generations of gold jewelry — bangles passed down from a grandmother, a mother’s wedding set, a daughter’s recent engagement chain. Total value, conservatively estimated, around fifteen lakh rupees.

The bank’s legal liability, under current Reserve Bank of India guidelines: roughly three lakh rupees. The remaining twelve lakh — a working-class family’s lifetime of careful saving — was simply gone.

This isn’t a hypothetical. Nor is it an isolated case. It’s the new reality of bank locker ownership in India after the RBI’s revised guidelines came into force on January 1, 2022. And it’s a reality most Indian families haven’t fully understood yet.

If you’re reading this from a coastal Andhra household where the family vault probably still leans on a bank locker — or worse, on a bedroom cupboard — the assumptions most families grew up with around “safe storage” have quietly changed since the RBI’s 2022 rules came into effect.

So What Changed, Exactly?

Until 2022, there was no real clarity in Indian law about how much responsibility a bank actually carried if something went wrong with a locker. Most families assumed — reasonably — that if the bank stored your gold and the bank got robbed, the bank would cover the loss fully.

That assumption was always more wishful than legal. In 2021, the Supreme Court of India directed the RBI to put proper guidelines in place. The RBI’s response, effective January 1, 2022, did clarify the rules — but not in the way most depositors hoped.

Under the revised guidelines, banks now carry a defined but capped liability for locker losses. Specifically:

| Cause of loss | Bank’s legal liability |

| Theft, burglary, fire (due to bank’s negligence) | Up to 100× the annual locker rent |

| Fraud by bank employees | Up to 100× the annual locker rent |

| Building collapse (bank’s negligence) | Up to 100× the annual locker rent |

| Floods, earthquakes, lightning | ₹0 — explicitly excluded |

| Customer negligence | ₹0 |

The hundred-times-annual-rent rule sounds large at first reading. Stretched against the actual value most Indian families store in a locker, it becomes uncomfortable arithmetic.

What The Numbers Look Like for an Indian Family

A typical medium-sized bank locker in a Tier-2 city like Visakhapatnam costs somewhere between ₹2,500 and ₹4,000 per year. That means the bank’s maximum legal liability sits between ₹2.5 lakh and ₹4 lakh — regardless of what’s inside.

Now consider what an average Indian family actually keeps in that locker:

Scenario A — Small household holding: A young couple’s combined wedding gold and daily-wear ornaments. Conservatively, around ₹5 lakh. Locker rent ₹2,500/year. Maximum bank compensation if the locker is burgled: ₹2.5 lakh. Net family exposure: ₹2.5 lakh.

Scenario B — Mid-sized family holding: Two generations of gold — wedding sets, festival jewelry, a few investment coins. Around ₹15 lakh. Same locker rent. Maximum compensation: ₹2.5 lakh. Net family exposure: ₹12.5 lakh.

Scenario C — Multi-generational household: Grandmother’s heirloom set, mother’s wedding gold, daughter-in-law’s wedding gold, festival accumulation across three decades. ₹50 lakh isn’t uncommon for established Tier-2 families. Net family exposure: ₹47.5 lakh — almost the entire value.

For most Indian middle-class families holding any meaningful gold, a bank locker now insures less than 30% of what’s inside it.

That gap — between what’s stored and what’s protected — is what the RBI’s 2022 rules have made explicit. The protection was always limited. The 2022 rules just put a number on it.

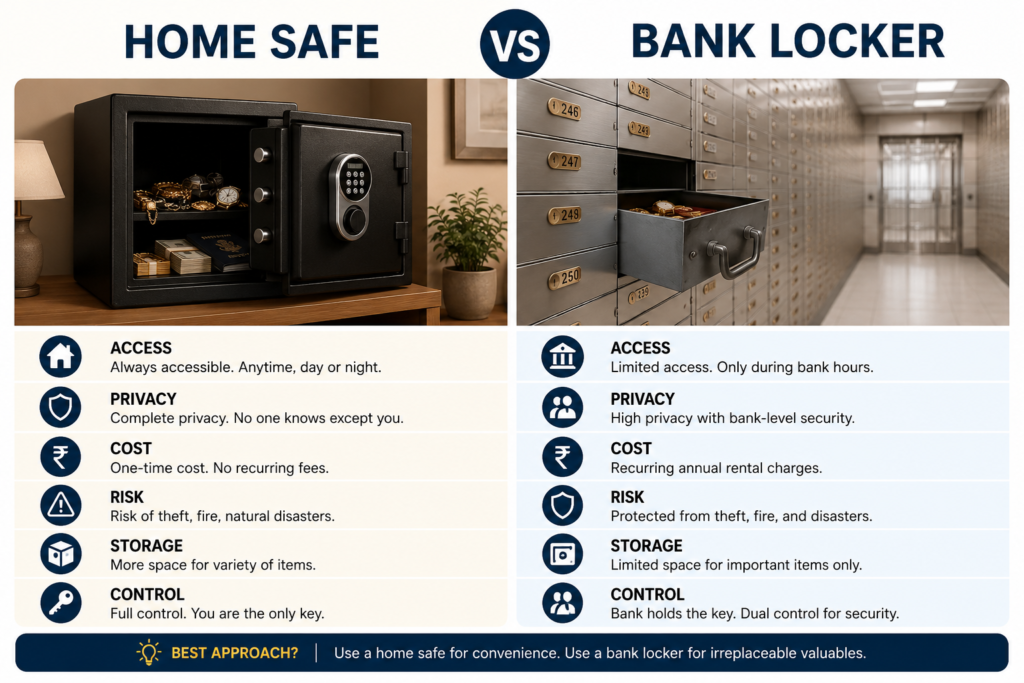

What Changes When Protection Stays At Home?

A certified home safe operates on a fundamentally different model. You’re not renting protection from someone else — you’re owning it directly.

A good home safe in the ₹50,000–₹2.5 lakh range, from a reputable manufacturer with proper certifications, offers several layers of coverage that a bank locker doesn’t:

Physical security that’s backed by manufacturer warranty. Brands like Godrej publish their construction grades — for example, the Advanced Series is rated 100× stronger than a wooden cupboard, and the Extreme Series is rated 250× stronger. These aren’t marketing numbers; they’re based on controlled in-house testing and ECBS certification for fire-resistant models.

Coverage of all loss categories. A home safe protects against fire, theft, natural calamities, and accidental damage — and combined with a home insurance rider, it can cover virtually every major loss scenario.

There’s also a practical difference many families don’t realise: banks aren’t supposed to know what’s inside your locker, which means they can’t insure the contents directly either. With a home safe, families can insure jewellery based on its declared value — something traditional lockers aren’t designed around under the 2022 rules.

Instant, private access that doesn’t depend on banking hours.No banking hours. No queue. No record of what you’re storing or when you accessed it. For a family that wears jewelry across festivals, weddings, and daily occasions, this matters more than we realize.

An asset that itself becomes heritage. A well-chosen home safe lasts decades. Your daughter inherits the contents and the safe.

The Indian market offers options across price bands. Compact units like the Godrej NX Pro Plus 45L start at around ₹36,000 for everyday valuables. Mid-tier options like the NX Advanced 210L (₹1.56 lakh) suit families with significant gold holdings. The premium Matrix and Extreme series (₹1.2 lakh to ₹2.4 lakh) are built for households where the protection itself becomes generational.

The Honest Trade-offs

In fairness, a home safe isn’t a perfect answer either.

It needs to be installed correctly — anchored to the floor or wall, placed thoughtfully (not in obvious locations), and ideally backed up by basic home insurance for very high-value contents. Biometric locks need backup key access, especially in humid coastal climates where electronic sensors can age faster over time. And for documents you may only need once in several years — old property papers, original deeds, a bank locker still has its place.

For most Indian families, the better approach usually isn’t “home safe instead of a bank locker.” It’s a more deliberate split: daily-access valuables and significant gold at home in a quality safe, while truly rarely-accessed documents stay at the bank.

The mistake is assuming everything kept in a bank locker is automatically fully protected. After 2022, that assumption is, mathematically, no longer correct.

For Vizag Families, The Question Has Quietly Changed

In coastal Andhra households, the typical mix — ancestral gold, wedding jewelry, property documents, festival accumulation — easily exceeds 100× any practical bank locker rent. The 2022 rules don’t change what you own. They just change what’s protected.

And for many families, that’s where the question has quietly shifted from “where do we keep it?” to “how much of it is actually protected if something goes wrong?”

That’s also why more Vizag families have started looking at home safes less like a luxury purchase, and more like long-term protection that stays within the house itself.

And for families trying to understand what level of protection actually fits their household, seeing the options in person often helps.

Kurveline Studio is the Authorized Partner of Godrej Enterprises Group for Safes and Home Lockers in Visakhapatnam. Our showroom at GK Towers, Dwaraka Nagar, has the complete Godrej range on display — from compact Pro Series units to the heavy-grade Extreme Series — so you can see, touch, and try them before deciding what fits your family’s actual holdings.

You’re welcome to explore the range in person. Bringing your typical gold holding sizes in mind often makes it easier to understand which level of protection fits your household best.

Visit us at GK Towers, Ground Floor, Shop No. 13–15, opposite Kalavaibhav Cellar, Dwaraka Nagar 1st Lane, Visakhapatnam. For queries or guidance, WhatsApp 9010788829. We’re open Monday to Saturday until 9 PM.

Kurveline Studio · Authorized Partner of Godrej Enterprises Group · Visakhapatnam

Instagram Carousel Adaptation

For when the blog gets cross-posted to Instagram. Same content, restructured for swipe-format.

Slide 1 — Hook (cover slide):

Bank Locker = Safe? Not Anymore. What RBI’s 2022 rules mean for your family’s gold. Swipe →

Slide 2 — Real story:

A Vizag family. ₹15 lakh of family gold in a bank locker. Locker burgled in February. Bank’s legal liability: ₹3 lakh. Their loss: ₹12 lakh. This isn’t hypothetical anymore.

Slide 3 — What changed:

RBI’s revised guidelines (effective Jan 1, 2022) capped bank liability at 100× the annual locker rent.

Theft, fire, employee fraud → covered up to that cap. Floods, earthquakes, lightning → ₹0.

Slide 4 — The math:

Average locker rent: ₹2,500–4,000/year. Maximum bank compensation: ₹2.5–4 lakh. Your typical family gold: ₹10–50 lakh.

For most Indian families, a bank locker insures less than 30% of what’s inside it.

Slide 5 — Scenario A:

Young couple, wedding gold: ₹5 lakh. Bank’s max liability: ₹2.5 lakh. Exposure: ₹2.5 lakh.

Two-generation family gold: ₹15 lakh. Bank’s max liability: ₹2.5 lakh. Exposure: ₹12.5 lakh.

Three-generation household: ₹50 lakh. Bank’s max liability: ₹2.5 lakh. Exposure: ₹47.5 lakh — almost everything.

Slide 6 — The alternative:

A certified home safe covers: ✅ Theft & burglary ✅ Fire & natural calamities (with insurance rider) ✅ Instant private access — no bank hours, no queue ✅ A lifetime asset that itself becomes heritage

Slide 7 — CTA:

See it before deciding.

Kurveline Studio · Authorized Godrej Partner 📍 GK Towers, Dwaraka Nagar, Vizag 💬 DM us for a free showroom demo 🕒 Open until 9 PM, every day

Caption for Instagram Post

The bank locker math has changed — and most Indian families haven’t done the calculation yet.

Since RBI’s 2022 rule update, banks are liable for only 100× the annual locker rent — meaning a typical ₹2,500/year locker now covers up to ₹2.5 lakh, even if there’s ₹50 lakh of family gold inside. 🔓

If you’ve never run this math on your own family’s situation, this carousel is worth a slow swipe.

Drop us a DM if you want to talk through what works for your family’s gold storage — or visit our Dwaraka Nagar showroom (Authorized Godrej Partner) anytime before 9 PM. Free demo, no pressure. ✨

#HomeSafeIndia #GodrejSafes #VisakhapatnamVizag #BankLocker #GoldProtection #FamilyGold #KurvelineStudio #DwarakaNagar #AuthorizedGodrejPartner #VizagFamilies #GoldSafety #RBIRules #GoldStorage #HomeSecurity #IndianFamilies

LinkedIn Adaptation Note

For LinkedIn, two adjustments to the same content:

Tone shift: Replace “Indian families” with “Indian households” or “Vizag households.” Replace “bedroom cupboard” with “informal storage.” More formal register, same substance.

Opening hook adjustment: LinkedIn favors business-context opens. Replace the family-burglary opener with something like:

Most Indian households still treat bank lockers as the default for storing gold and important documents. After the RBI’s January 2022 rule update, that default is mathematically less defensible than most depositors realize. Here’s the math, run for typical Tier-2 holdings, and what it means for the way Indian families are starting to think about home security.

Posting account: Publish from Pravin Kumar’s personal LinkedIn rather than Kurveline’s company page. LinkedIn’s algorithm gives personal articles 3–5× the reach of company-page articles. Use Kurveline as a tagged company.